Check out our latest articles.

The first step to better financial decisions is to learn more about your money!

Filter

Cancel

Done

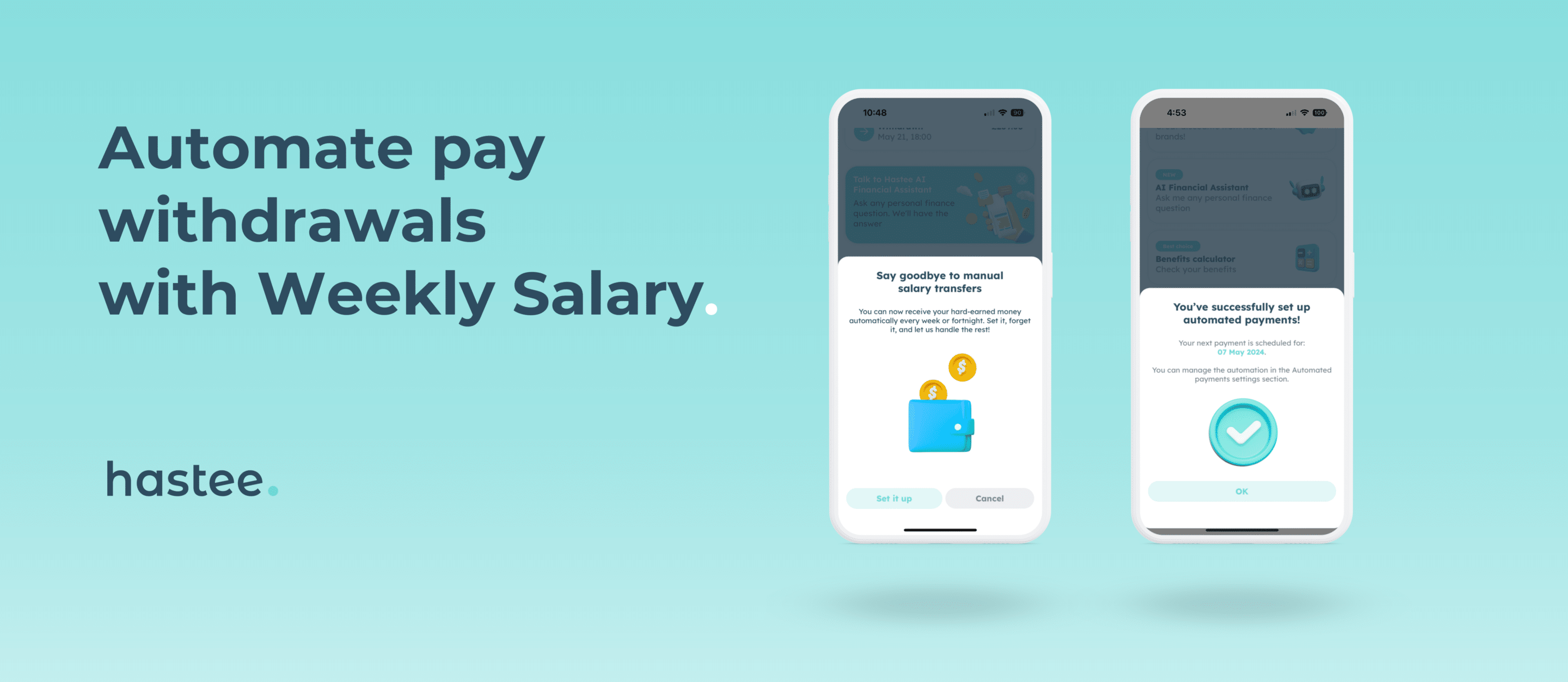

At Hastee, we understand that the financial wellbeing of your employees is crucial to their overall satisfaction and productivity. That’s why we’re excited to introduce our latest feature, Weekly Salary—a powerful tool designed to help you better support your workforce by automating their pay withdrawals on a weekly or fortnightly basis. What is Weekly […]

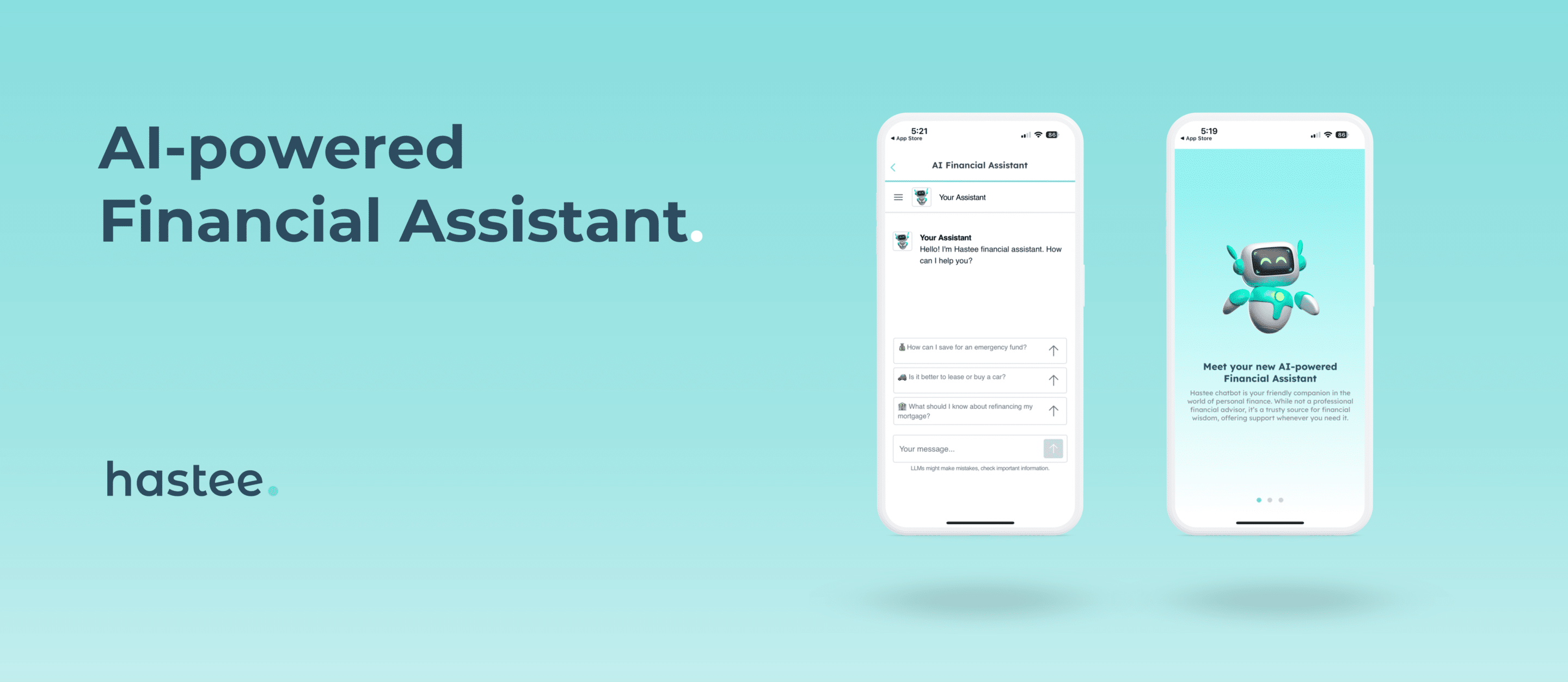

Let us introduce you to the groundbreaking AI Financial Assistant! This innovative addition to Hastee’s suite of services is set to revolutionise the way you manage your personal finances. What is the AI Financial Assistant? The AI Financial Assistant is a free and confidential AI-powered chatbot designed to answer all your personal finance questions. […]

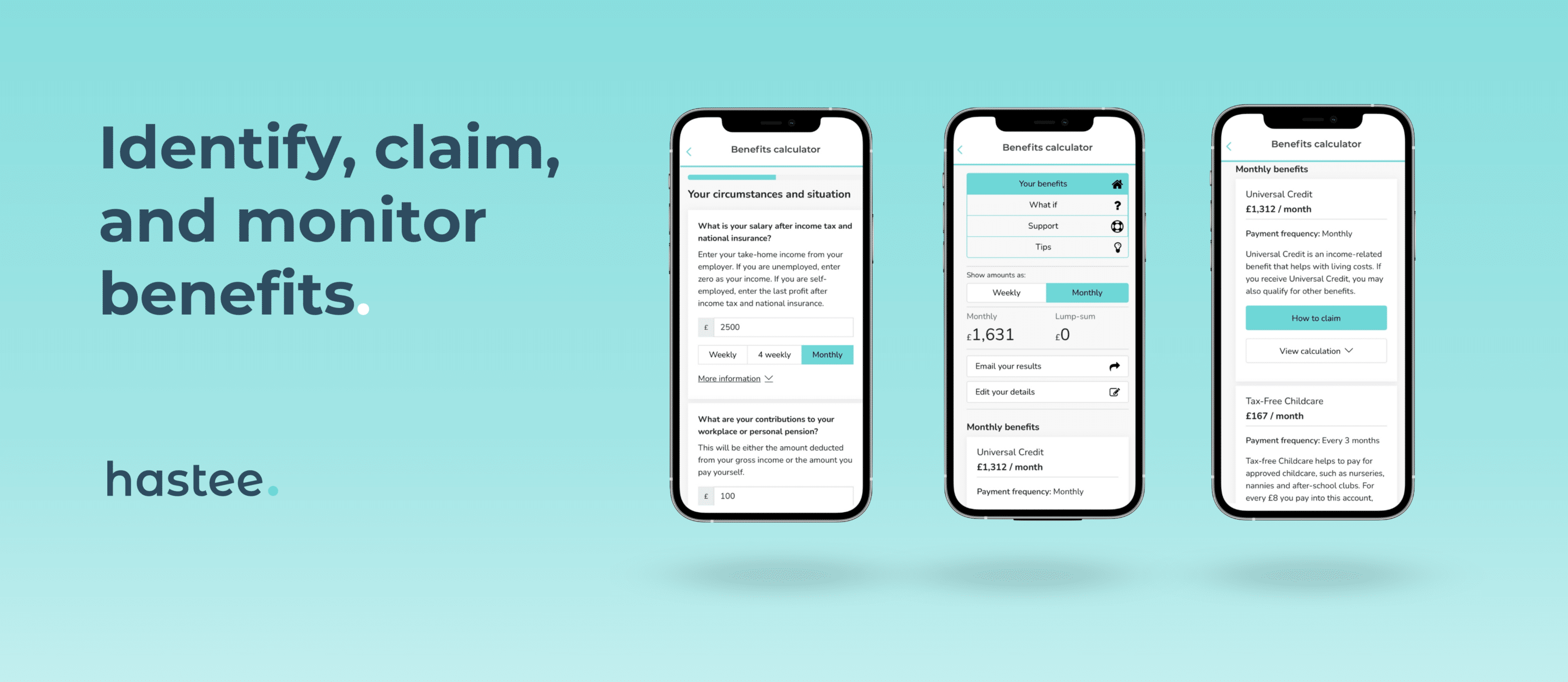

Many people wrongly assume that they are not eligible for benefits or think that the application is too complicated. In reality, this is not the case; 8 million households are just a few taps away from claiming £19 billion in benefits. In fact, if you’re earning less than £60,000, you could well be eligible. To […]

The cost-of-living crisis in the UK is still hitting both hospitality businesses and their employees hard. As operational costs rise and consumers tighten their belts, hospitality businesses face the dual challenge of maintaining profitability while ensuring their staff are adequately compensated. Polaris Elements and Hastee have come together to offer some insights, addressing both the […]

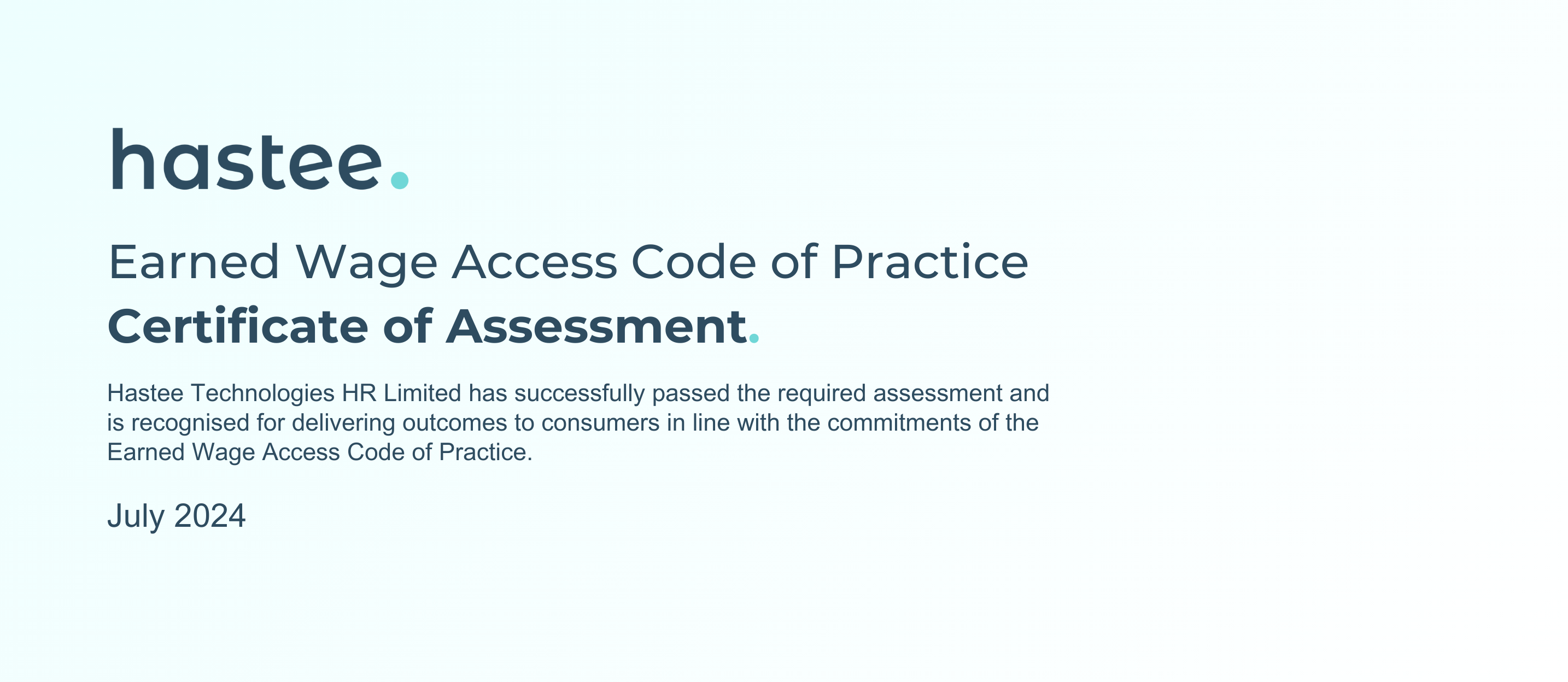

Pioneering Success: Hastee Achieves Landmark Compliance with EWA Code of Practice Back in 2023, Hastee joined forces with the UK Money & Pensions Service, the CIPP, and 6 other Earned Wage Access (EWA) providers to launch the world’s first ‘EWA Code of Practice’. The Code set out a common standard that firms providing EWA products […]

As the corporate landscape evolves, more companies are aiming to enhance the number and variety of benefits they offer to their employees. Traditional social benefits such as health insurance, meal vouchers, and transportation vouchers are becoming standard. But the benefits that are truly setting companies apart today go beyond these basics. In the modern workplace, […]

Author: Manu Peleteiro, CEO at Inbest.ai There are over 8mn vulnerable households not claiming benefits because they wrongly assume that they are not eligible or think that the application is too complicated. The most common reasons people assume they are not eligible is because they believe that their income is too high, or they wrongly […]

Celebrating the Unbeatable Hastee Team Spirit! Have you ever witnessed a team that radiates enthusiasm, creativity, and unwavering unity? Well, you’re about to as we take you through our recent Castelldefels off-site extravaganza with the absolutely fantastic Hastee team! 🌞🌴 A Team Like No Other What makes a team truly amazing? It’s not just about […]

Hastee joins forces with the UK Money & Pensions Service, the CIPP, and 6 other EWA providers to launch the world’s first ‘EWA Code of Practice’ Earned Wage Access (EWA) is growing rapidly all around the world: giving employees access to their earned pay has now become a legal requirement in counties such as Spain, […]

Many people wrongly assume that they are not eligible for benefits or think that the application is too complicated. In reality, this is not the case; 8 million households are just a few taps away from claiming £19 billion in benefits. In fact, if you’re earning less than £60,000, you could well be eligible. To […]

We are all guilty of getting sucked into a sale or purchasing something we probably could’ve gone without. But in that moment of time we know it is wrong, but that rose quartz drink bottle to positively charge your water, just felt so right. At a time when many retailers are aiming to boost online […]

Well if Earned Wage Access, isn’t a benefit then what is it? It’s the future. In its simplest form, most people are paid fortnightly or monthly (mostly the latter here in the UK) and we are removing this barrier, allowing workers to access a portion of their earned wage, when they need it. Earned Wage […]

The term ‘destination employer’ is a badge of honour for any business, but one does not simply become a destination employer overnight. Whether a business qualifies as one depends on how jobseekers and your existing staff perceive the business. If you’re seen as a company that is well known and respected in your industry and […]

“Switching to Hastee has given us unparalleled peace of mind and happier employees” – Beatriz Andueza Rodriguez, Head of Personnel at Securitas Direct Securitas Direct, a leading security company in Spain and Portugal with over 10,000 employees, recognised the need for more immediate financial support options for their staff, so they turned to Hastee. Over […]

Who do you work for? I work for GMS Security as Business Protection for Jaguar and Land Rover. I have been working with GMS now for 5 months and I really enjoy working with the team here, as every day is different. What do you like about being able to get paid weekly? Without […]

How do you prefer to start your day? I love to start it by going to my favourite coffee shop next to my house, there’s nothing I like more than reading the newspaper while enjoying the best coffee in Barcelona! What was your first job? It was while I was in high school with 17 […]

Pioneering Success: Hastee Achieves Landmark Compliance with EWA Code of Practice Back in 2023, Hastee joined forces with the UK Money & Pensions Service, the CIPP, and 6 other Earned Wage Access (EWA) providers to launch the world’s first ‘EWA Code of Practice’. The Code set out a common standard that firms providing EWA products […]

Celebrating the Unbeatable Hastee Team Spirit! Have you ever witnessed a team that radiates enthusiasm, creativity, and unwavering unity? Well, you’re about to as we take you through our recent Castelldefels off-site extravaganza with the absolutely fantastic Hastee team! 🌞🌴 A Team Like No Other What makes a team truly amazing? It’s not just about […]

Hastee joins forces with the UK Money & Pensions Service, the CIPP, and 6 other EWA providers to launch the world’s first ‘EWA Code of Practice’ Earned Wage Access (EWA) is growing rapidly all around the world: giving employees access to their earned pay has now become a legal requirement in counties such as Spain, […]

Many people wrongly assume that they are not eligible for benefits or think that the application is too complicated. In reality, this is not the case; 8 million households are just a few taps away from claiming £19 billion in benefits. In fact, if you’re earning less than £60,000, you could well be eligible. To […]

With an amazing shortlist of the UK’s best fintech co’s such as Chip, LOQBOX, Plum, Snoop, and Tickr, Hastee came out victorious. A massive team effort and we are hugely proud of each and everyone of the team to put Earned Wage Access at the forefront of the UK Fintech scene. The Judges said: […]

Acquisition consolidates leading ‘flexible pay’ provider to benefit all sizes of customer and accelerate the modernisation of pay LONDON, UK, 12th November, 2020: Hastee, the leading earnings on demand company, has agreed to acquire Typs, their Spanish counterpart, to accelerate growth across Southern Europe and beyond. The deal combines two leading Earnings on […]

We’d love to introduce you to our brand spanking new CEO, Jaime Jimenez. This week we sat down with him to ask the hardest of the hard hitting questions. You’re welcome! ✨Slack or Emails? Emails… does that mean I am old school? ✨Circles or squares? Squares ✨Be chased by 10,000 scorpions or 10 lions? 10 […]

Hastee was founded for a purpose: to improve the financial health and productivity of workers. Our solution allows employees to withdraw a portion of their pay as soon as they have earned it, breaking the outdated monthly pay-cycle that forces many into debt and financial stress. Today we’re excited to announce we are one of the 14 […]

We are excited to announce an exclusive partnership with leading health and wellbeing benefits provider Vivup. Hastee, who enable employees to access a portion of their earned pay when they need it, are already established within healthcare, working with NHS Trusts including South London and Maudsley NHS Trust, leading Care Home provider Bluebird Care and […]

LONDON, UK., 27th April 2021: Hastee, the award-winning, financial health platform, has today announced an exclusive new partnership within the Earned Wage Access space , with global financial wellbeing platform nudge, which will allow Hastee users access to its financial education and money management tools within the Hastee app. Hastee nurtures employee financial health […]

As the corporate landscape evolves, more companies are aiming to enhance the number and variety of benefits they offer to their employees. Traditional social benefits such as health insurance, meal vouchers, and transportation vouchers are becoming standard. But the benefits that are truly setting companies apart today go beyond these basics. In the modern workplace, […]

Author: Manu Peleteiro, CEO at Inbest.ai There are over 8mn vulnerable households not claiming benefits because they wrongly assume that they are not eligible or think that the application is too complicated. The most common reasons people assume they are not eligible is because they believe that their income is too high, or they wrongly […]

If your child has a disability or long-term health condition, you might be entitled to Disability Living Allowance (DLA) for them as well as other financial support. This page explains more about the disability benefits and entitlements your child might qualify for and how to claim them. Disability Living Allowance Personal Independence Payment (PIP) Help […]

If you’re already getting certain benefits and need a loan, see if you can apply for an interest-free Budgeting Loan from the Social Fund. This can be much cheaper than paying high interest charges for borrowing from payday or doorstep lenders. This page tells you how Budgeting Loans work and how to apply for them, […]

When it comes to spending, borrowing and avoiding charges, each type of payment card has different pros and cons. This guide tells you more about the main options. Cards for borrowing, cards for spending Credit cards Debit cards Store cards Prepaid cards Charge cards Credit builder cards Cards for borrowing, cards for spending There are […]

If your bank, building society or credit union went bust you would be entitled to compensation through the Financial Services Compensation Scheme for a maximum of £85,000. Find out what happens for joint accounts and if you have money with two banks in the same banking group. What is the Financial Services Compensation Scheme (FSCS)? […]

You have javascript turned off. Please turn javascript on to see the tools in action. Calculate your monthly mortgage payment

You have javascript turned off. Please turn javascript on to see the tools in action. Savings Calculator

View More

View More

No View More

No results found.

We couldn’t find what you searched for. Please try again.